Data Leak, Demographics, and Consumption

How China overcounted its population and the myth of consumption-led growth

The Setup:

The elements of today’s post — China’s 2020 census overcounting, the Shanghai data leak, and the consumption-led growth story — have been publicly available for a while now. We thought we’d tie the threads together and make their implications more explicit.

Contents:

1. An Obstetrician’s Take on Official Census Data

Yi Fuxian is an obstetrics and gynaecology researcher at the University of Wisconsin-Madison and the author of Big Country with an Empty Nest, published way back in 2013. Here’s his 2022 commentary on China’s census data, where he lays out his logic for adjusting the official population figures:

[… the] Bacille Calmette-Guérin vaccination (against tuberculosis) is mandatory in China for every newborn within 24 hours of birth, and we know that an average of 1.2-1.5 newborns can be vaccinated with one dose of BCG (from one newborn in small hospitals to as many as three in large hospitals). For example, because 11.54 million doses of BCG were distributed in 2010, and the 2010 census showed 13.79 million people aged 0, then an average of 1.2 newborns were vaccinated per dose.

In 2018, 2019, and 2020, the numbers of BCG doses distributed were 6.21 million, 5.73 million, and 5.37 million, respectively. That means China’s population began to decline in 2018 (when deaths totaled 9.93 million), and it suggests that China will soon have fewer births per year than Nigeria and Pakistan. […]

Yet, according to the 2022 WPP’s [i.e. UN] population figures for 2018, 2019, and 2020, each dose of BCG would had to have been stretched out to 2.7, 2.6, and 2.5 newborns, respectively. That defies medical common sense.

Yi Fuxian’s adjusted population structure for China is in black. It’s clearly well below the other sources (i.e., China's official data and UN estimates), especially for the younger cohorts. From what we can tell, his adjustment is based purely off the vaccination data argument.

*Full disclosure, our obstetrician gained a fair amount of notoriety on the mainland, with China Central Television accusing him of creating rumours and the People’s Daily Online ranking his argument third in its “Top Ten Rumors of 2019 in China”.

2. Shanghai Police Data Leak

In June 2022, hackers claimed to have breached data on 1 billion Chinese citizens sitting on the Shanghai police servers. The data cache was put up for sale for 10 Bitcoins. The hackers also released a data sample on 250,000 household registrations, all dispersed and random, covering almost every county in the country.

Since sampling is not perfectly uniform, it is not possible to pinpoint the number of people in each age group nationwide; but the overall pattern of the age distribution is consistent with past censuses. It suggests that post-1990 births continued to decline faster than I had predicted […]. That means China’s real population is not 1.41 billion (the official figure) and could be even smaller than my own estimate of 1.28 billion. It also means that China’s economic, social, foreign, and defense policies – as well as those of the United States and other countries toward China – are based on erroneous demographic data.

In short, Yi Fuxian’s prior population structure estimate (adjusted using vaccination data) broadly matches that of the Shanghai police leak.

This means we now have two separate and independent methods of adjusting the official census data, and both of these show dwindling numbers in the younger cohorts.

China’s ageing way faster than we previously thought.

3. Implications: The Myth of Consumption-Led Growth

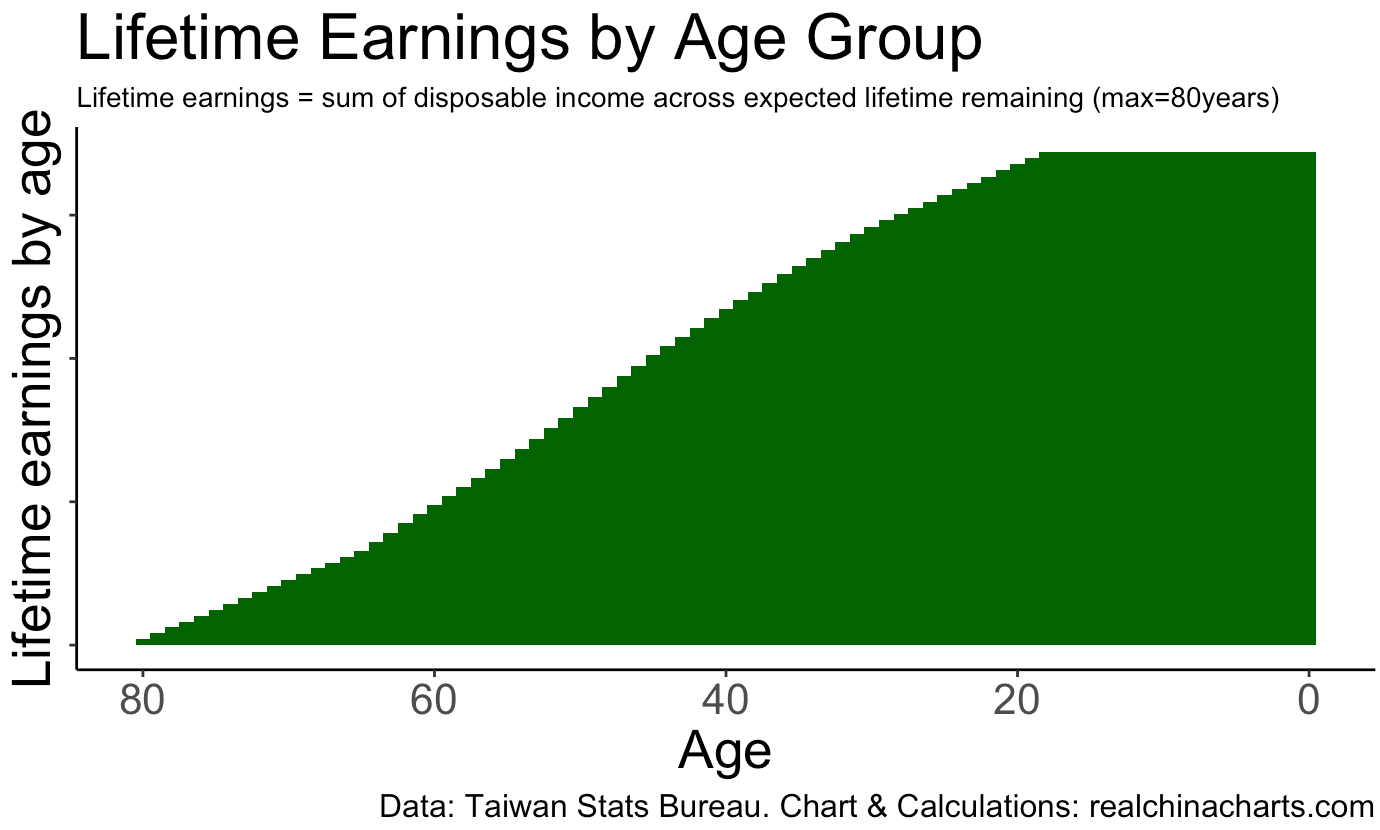

Here’s the fun bit and our own value-add for this post. We take the population structure from the Shanghai police leak curve and adjust it by the disposable incomes by age group. As China doesn’t publish such detailed data, we take Taiwan’s Statistical Bureau data as a proxy for income (conceptually similar to this chart in the US). Since we aren’t looking at absolute currency values but rather the differences in income and spending power between age groups, this is fine. We then sum the product of each age cohort’s remaining life expectancy years (~80 years) (e.g. a 30-year-old in 2020 has, on average, 50 years left to earn and spend) and their disposable income across those remaining years. Long story short, we arrive at the chart above.

The feasibility of consumption-led growth is gone. The ship has sailed, and the window has closed for any potential reforms. China’s demographics, even adjusted by lifetime earnings, are stepping off the cliff literally this year (2023). It’s an inflexion point.

The significantly lower population counts in these younger cohorts mean that even if the young would hypothetically earn more than their parents on average (more on that later in the post), this will not compensate for their lower numbers.

Going forward, all Chinese consumer groups above 30 years of age as of 2020 (or 33yo as of 2023) will have lower disposable income in the aggregate than previous cohorts. It’s not an up-and-to-the-right perpetual growth story anymore.

For those who would like to see the lifetime earnings curve we used to make the adjustment, here it is in green above. Notice that 80yos have near zero earnings/spending power left, whereas the youngest cohorts have the highest. Children under 18 years of age are flat since they do not earn yet but have latent potential prior to reaching adulthood.

We add wage growth as another adjustment factor into the calculations. We now have three factors in the calculation: population structure * lifetime earnings * wage growth.

To compensate for the demographic cliff, China would have to achieve sustained real wage growth of ~9% year-on-year to maintain consumer earning and spending power levels.

Historical data from Bloomberg shows the most recent print for nominal median wage growth at ~4.7% and falling.

Thanks for reading! If you enjoyed this post, please consider supporting us via a subscription or circulating our writing among your professional circle.

We are a pair of finance professionals with an interest in China. We love putting out China Charts. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford the subscription, please hit the button and pick one of the three options.

Can you guys comment on Yi’s analysis of the leaked police data? Do you think his methodology is valid?